Income Protection Insurance for Doctors

Income Protection Insurance for Doctors

Income protection insurance for doctors: a comprehensive guide

Doctors are often assumed to be financially secure. High income, stable career, respected profession — from the outside, it looks like a solid foundation. But there is one critical vulnerability that is easy to overlook: everything depends on your ability to work. An unexpected illness, injury, or mental health crisis can stop that income overnight, and the financial consequences for a high-earning professional with significant commitments can be severe.

What is income protection insurance?

income protection insurance is designed to replace a portion of your usual income — typically up to 70% plus your super guarantee contributions if you are unable to work due to illness or injury. It provides a crucial financial buffer during recovery, helping to cover lost income for an extended period.

Key features include:

- Benefit period — payments can continue from 2 years up to age 65, depending on your policy

- Waiting period — a period before payments begin, typically ranging from 30 to 90 days

- Coverage scope — most policies cover both total and partial disabilities, including physical and mental health conditions

Income protection insurance is a critical safety net — not a luxury — for the financial security of doctors and healthcare workers.

Why doctors need it more than most

A larger income means a proportionally larger financial gap when earnings suddenly stop. Mortgage repayments, practice costs, and investments don't pause.

Medicine rarely offers a reduced-capacity alternative. Even minor conditions — a hand injury, anxiety, or early burnout — can prevent a doctor from working in their specialty entirely.

Centrelink is means-tested and entirely inadequate for a doctor's obligations. Workers' compensation applies only to workplace injuries.

Doctors experience disproportionately high rates of burnout, depression, and anxiety — all leading causes of income protection claims in the profession.

Many doctors work as contractors or practice owners with no sick leave or employer-funded income continuance. Income protection fills this gap entirely.

Years of training and HECS/HELP debt mean peak earning years arrive much later. Income disruptions early in a career have lasting consequences on long-term financial security.

What to look for in a policy

Not all income protection policies are equal. For doctors, the following features are particularly important to consider when choosing a policy:

- Own-occupation definition of disability — you can claim if unable to perform your specific medical specialty, even if technically capable of another role. A surgeon with a hand injury would still receive benefits even if they could consult or teach. Without this, your claim may be denied if you can perform any work at all.

- High replacement ratio — look for policies replacing up to 70–75% of your pre-tax income

- Any-occupation definition of disability — Once the ‘Own’ occupation definition is exhausted the cover continues under an ‘Any’ occupation. This definition specifically reviews whether you can work in ‘Any occupation for which you have qualifications, part work experience, skills and re-training potential.

- Extended benefit period — seek coverage through to age 65 or 70 where possible, rather than a short fixed term, for long-term financial security

- Waiting period suited to your cash flow — typically 30–90 days; choose one that aligns with how long your reserves can sustain your expenses

- Mental health coverage without restrictive limits — avoid policies that impose short benefit periods or low caps on mental health claims

- Medical-specific features — look for Needlestick Benefits or cover for blood-borne diseases such as HIV or Hepatitis

- Tax deductibility — income protection premiums are often tax deductible, which can significantly reduce the overall cost, particularly for those in higher tax brackets

- Super fund options — Default coverage included in your super fund is not an underwritten contract of insurance which can result in lengthy or denied payments at claim time. Make sure you have an underwritten contract even if funding through super.

Exclusions and limitations to watch out for

Exclusions are specific situations where your policy will not pay out, while limitations restrict the amount or duration of cover. Common exclusions include pre-existing conditions, self-inflicted injuries, and illnesses sustained during high-risk activities.

For medical professionals, it is especially important to check whether your policy covers needlestick injuries or infectious diseases, as not all policies treat these the same way. Some policies also impose shorter benefit periods or lower limits specifically for mental health claims.

Always review the Product Disclosure Statement (PDS) in full before committing to a policy. This document outlines all exclusions and limitations and will help you avoid surprises at claim time.

Assessing the financial strength of your insurer

Your policy is only as reliable as the company standing behind it. To assess an insurer's financial strength, check their credit rating from independent agencies such as Standard & Poor's or Moody's. A high rating signals the insurer is well-positioned to meet its obligations, even during challenging economic periods.

Consider the insurer's claims payment history, customer service reputation, and ownership structure — whether they are a standalone company or part of a larger financial institution, which can provide additional backing and stability for long-term cover.

A real-world example

An orthopaedic surgeon in their mid-forties with a busy private practice sustains an unexpected back injury — making it impossible to perform surgery. Without income protection, they face immediate pressure on their mortgage, practice overheads, and personal expenses, with no clear recovery timeline.

With an own-occupation income protection policy in place, they receive 70% of their pre-tax income throughout their recovery period. Their financial commitments are met, their assets remain intact, and they can focus entirely on rehabilitation without the compounding stress of financial hardship.

If they were to become permanently disabled and unable to return to their profession, the policy provides ongoing coverage to safeguard their long-term financial security. This illustrates why the details of a policy — particularly the own-occupation definition — matter enormously at claim time.

Your dedicated income protection insurance broker

Income protection for medical professionals is a specialist area. Policies vary significantly in how they define disability, what they exclude, and how claims are assessed. Kat has over 20 years of experience in the financial and insurance industry and works with doctors and healthcare professionals across Australia.

Katarzyna Urbanik

Director of Morgan Insurance — Senior Risk Adviser — Life Insurance, Income Protection, Trauma, TPD, Key Person Insurances

- Bachelor of Business

- Diploma of Financial Planning (RG146)

- Advanced Diploma Financial Services

- Tier 2 General Insurance Compliance

Final thoughts

Income protection insurance does far more than replace a paycheque. For Australian doctors, it protects the years of training and sacrifice invested in building a career, provides stability during recovery, and helps preserve long-term financial security.

The profession's physical and cognitive demands, limited government support, and the realities of self-employment or contracting make income protection not just useful — but essential. The right policy, structured correctly, ensures that a health setback does not become a financial crisis.

Protect the income your career depends on

Get personalised advice tailored to your specialty, practice structure, and financial situation.

Get a quoteReferences

- ASIC MoneySmart – Income Protection Insurance: moneysmart.gov.au

- APRA – Individual Disability Income Insurance Statistics: apra.gov.au

- Financial Services Council (FSC) – Income Protection Industry Standard

- AIHW – Health Workforce Data, Medical Practitioners: aihw.gov.au

- Beyond Blue – National Mental Health Survey (Doctors and Health Professionals): beyondblue.org.au

- Safe Work Australia – Work-related Injury and Illness Statistics: safeworkaustralia.gov.au

Income Protection for over 50s

As we get older, our financial needs and priorities shift. For individuals over 50, having a stable income becomes increasingly vital, whether you’re nearing retirement or still working. Income protection insurance can serve as a crucial safety net, offering financial stability and peace of mind. Here’s why it’s so important:

Financial Security in Uncertain Times

Life is unpredictable, and health issues or accidents can occur at any age. For those over 50, the risk of illness or injury can be higher, potentially impacting their ability to work. Income protection insurance ensures that you have a steady income if you are unable to work due to a medical condition. This financial support can cover daily living expenses, medical bills, and other essential costs, allowing you to focus on recovery without the added stress of financial worries.

Maintaining Your Standard of Living

As you approach retirement, maintaining your standard of living is crucial. Income protection insurance helps bridge the gap between your current earnings and any potential loss of income due to illness or injury. This means you can continue to enjoy your lifestyle, pay your bills, and support your family, even if you are unable to work for an extended period.

Protecting Your Retirement Savings

For many over 50, retirement savings are a critical component of their financial plan. Without income protection insurance, you might be forced to dip into your retirement savings to cover expenses if you are unable to work. This can deplete your nest egg and jeopardise your financial security in retirement. Income protection insurance helps safeguard your retirement savings by providing an alternative source of income during times of need.

Peace of Mind for You and Your Family

Knowing that you have a financial safety net in place can provide immense peace of mind. Income protection insurance not only supports you but also ensures that your family is taken care of. This security allows you to focus on your health and well-being, knowing that your loved ones are financially protected.

Tailored Coverage Options

Income protection insurance policies can be tailored to meet the specific needs of those over 50. Whether you are still working full-time, part-time, or transitioning into retirement, there are policies designed to fit your unique situation. Working with an experienced insurance advisor can help you find the right coverage that aligns with your financial goals and lifestyle.

Conclusion

Income protection insurance is a crucial consideration for individuals over 50. It provides financial security, helps maintain your standard of living, protects your retirement savings, and offers peace of mind for you and your family. By investing in income protection insurance, you can ensure that you are prepared for any unexpected events that may impact your ability to work, allowing you to enjoy your later years with confidence and security.

If you have any questions or need assistance in finding the right income protection insurance policy, feel free to reach out to us. We’re here to help you secure your financial future.

Get a Quote

Understanding Accidental Life Cover: What You Need to Know

Accidental Life Cover is a type of insurance that provides a lump sum benefit to your beneficiaries if you pass away due to an accident. For a claim to be successful, the event must be deemed unplanned or unforeseen, resulting in accidental death. This type of cover is designed to offer financial support to your loved ones during a difficult time.

What Does Accidental Life Insurance Cover Include?

Your policy schedule will specify the amount of coverage you have under Accidental Life Insurance Cover. This lump sum can be used by your beneficiaries to pay off debts such as a home loan or credit cards. Additionally, it can help cover future financial needs, including school fees, daily living expenses, and the costs associated with raising children.

One of the main advantages of Accidental Life Cover is its affordability. Since it only covers specific circumstances—namely, accidental death—the premiums are generally lower compared to a standard Life Cover policy. However, this also means that the coverage is less comprehensive.

Coverage Details of Accidental Life Cover

What is Covered:

- Death caused by an Accident: Yes

What is Not Covered:

- Death caused by an Illness: No

- Partial Disability caused by Illness or Accident: No

- Total Disability caused by an Accident: No

- Total Disability caused by an Illness: No

- Serious Injury Caused by Accident: No

Common Exclusions in Accidental Life Cover

Accidental Life Cover policies often have specific exclusions. These may include:

- Working at heights

- Working underground

- Unlawful or criminal acts

- Aerial flying, unless as a passenger operated by a licensed pilot or airline

- Hazardous recreational activities, such as motor sports, base jumping, rock climbing, and certain contact sports

- Self-inflicted acts that cause death

- Mental illness

- Joining the armed forces

Conclusion

Accidental Life Cover can be a valuable addition to your insurance portfolio, providing financial security for your loved ones in the event of an accidental death. However, it’s important to understand the limitations and exclusions of this type of policy. By knowing what is and isn’t covered, you can make an informed decision about whether Accidental Life Insurance Cover is right for you.

If you need more information or further assistance, feel free to reach out to Morgans Insurance Advisors as your preferred life insurance broker for an obligation-free consultation. We’re here to help you navigate your insurance options and find the best coverage for your needs.

Underwritten versus Default Insurance: Ensuring Peace of Mind

When you pay for life insurance premiums, you deserve the peace of mind and security that comes with knowing your policy will protect you and your loved ones when it matters most. The last thing you want is to face unexpected obstacles or a denied claim during a critical time. This is why having confidence in your Life Insurance, Total and Permanent Disability (TPD), Trauma, and Income Protection Insurance cover is essential. After all, you are investing in these policies to ensure you are adequately insured.

The Importance of Completing Your Underwriting Upfront

One of the key benefits of underwritten insurance is the upfront completion of the underwriting process. This means that from the start, you will know exactly what your policy covers. If you have any past health issues that could affect a claim, an underwritten policy will clearly outline any exclusions. This transparency allows you to understand your coverage fully and avoid surprises later on.

Once your policy is underwritten, any future changes in your health or occupation will not impact the original terms of your contract. This means that unforeseen circumstances will not negatively affect your insurance cover or premiums, providing you with long-term stability and security.

Timing of Claims Assessment: A Crucial Difference

The timing of the claims assessment is a significant difference between default insurance and underwritten insurance. With underwritten insurance, the assessment is done upfront. Your policy is either accepted with standard terms or with special terms, which are clearly outlined in your contract. This applies to Life Insurance, TPD, Trauma, and Income Protection.

In contrast, default insurance, often provided automatically through super funds, is assessed at the time of the claim. This can lead to uncertainty and potential difficulties when making a claim. If you are in good health and younger, it may be more beneficial to secure an underwritten insurance contract. This proactive approach ensures that you are not paying for insurance that might be challenging to claim or could be denied when you need it most.

Conclusion

Choosing between underwritten and default insurance is a critical decision that can impact your financial security and peace of mind. By opting for underwritten insurance, you gain clarity, stability, and confidence in your coverage. Understanding the terms and conditions of your policy upfront allows you to make informed decisions and ensures that you and your loved ones are protected when it matters most. Investing in underwritten insurance is a proactive step towards securing your future and avoiding the pitfalls of default insurance policies.

Comparing Income Protection Insurance

When searching for Life Insurance, Total and Permanent Disability (TPD), Trauma, and Income Protection insurance, the cost is just one factor to consider. Different insurance companies may offer better rates depending on your age and occupation. However, the terms offered by different insurers can be even more crucial, especially when it comes to income protection or TPD cover.

Occupation Ratings and Terms Differ Across Insurers

When it comes to insurance, your occupation plays a crucial role in determining your overall risk and the premiums you pay. Insurance companies use your job as a key factor in their risk assessment process, which not only influences your premiums but also the specific terms of your insurance contract.

For instance, if you are a ‘White Collar’ worker, some insurance companies may allow you to return to work from day one following a disability or illness without affecting your ‘waiting period.’ This means you can continue working without having to wait for a certain period before your insurance benefits kick in. On the other hand, some super funds have stricter requirements. They may stipulate in their product disclosure statements that ‘White Collar’ workers must experience 14 days of total disability before they are eligible to make a claim under their income protection products. If this condition is not met, your claim could be denied.

Underwritten Cover

Another important consideration is whether you have underwritten insurance cover.

Underwritten cover refers to an insurance policy that has been fully assessed and approved by the insurance company based on your individual risk factors. This process involves a thorough evaluation of your personal information, such as your health, occupation, lifestyle, and medical history. Here’s why underwritten cover is important:

Greater Certainty and Stability

When you have a fully underwritten insurance policy, it means that the terms of your contract are fixed and agreed upon at the time of underwriting. This provides greater certainty because the insurance company cannot change the terms of your policy later on. You can rely on the definitions and conditions outlined in the product disclosure statement that was in effect when you took out the policy.

Default Cover

In contrast, a default insurance contract (often offered automatically through your super fund) may be subject to changes as the product disclosure statement of your provider evolves over time. It’s important to note that the same insurance company may provide different versions of their product disclosure statement depending on whether you apply for cover directly with the insurance company or via a third-party offering, such as a super fund.

General Advice

The information in this blog contains general information only. We have not taken into consideration any of your personal objectives, financial situation, or needs. Before taking any action, you should consider whether the general advice contained in this blog is appropriate for you, having regard to your situation or needs. We recommend consulting a licensed or authorised financial adviser if you require financial advice that takes into account your personal circumstances.

Morgan Insurance Advisors Pty Ltd is an Authorised Representative (ASIC No 319449) of HAE Financial Pty Ltd AFSL 501891.

Income Protection vs Workers Compensation Australia — Which Do You Need?

Is Income Protection Better Than Workers Compensation in Australia?

When it comes to keeping a roof over the head and food on the table if things go wrong, Workers Compensation and Income Protection Insurance get thrown into the mix, but they do very different things – and it’s the difference between them that could make all the difference in the long run.

What Workers Compensation Actually Covers

Workers Compensation is a state-run scheme, so the rules are different depending on where you live and work. So for example in New South Wales a claim is only valid if you hurt yourself on the job or at a work-related event. Which means in practical terms, if you get hurt at home, on the weekend or on holidays, you are pretty much on your own.

The Gap is a Big Problem

And it’s a problem because most accidents and injuries in Australia happen outside of work hours. Slipping in the backyard, a sporting injury, a nasty illness or a car crash on a Saturday arvo — none of these are covered by Workers Compensation. And that leaves most Australians with a hole in their financial protection that they probably didn’t even know was there.

How Income Protection Fills the Gap

Income Protection Insurance is a policy that pays you a benefit (usually about 70% of your pre-tax income) if you can’t work because of a covered condition – no matter where or how you get hurt. So if you’re knocked off your bike on the way home from work, or get sick with a nasty bug, or have a car accident on the highway, then your policy kicks in after your chosen waiting period.

Which makes Income Protection a much safer safety net for most Australians, especially those with a mortgage, family to support or limited savings to fall back on.

Do You Still Need Workers Compensation?

Well yes, you’re pretty much stuck with Workers Compensation if you’re an employee – it’s provided by your employer and it’s mandatory, so you don’t have a choice. But it’s not enough on its own. Income Protection fills in the gaps where Workers Compensation leaves you exposed, so you’re covered for all the things that can go wrong in life.

Which One Is Right for You?

If you’re an employee, you’ll already have Workers Compensation but you really should look at your Income Protection options as well. And if you’re self-employed then Workers Compensation might not apply to you at all, so Income Protection is even more essential.

Getting some advice from an personal insurance broker is the best way to figure out exactly where you stand and where you’re exposed.

Get a Quote

How Does Life Insurance Work?

Life cover revolves around a fundamental concept, yet not all life insurance policies are created equal. Here’s what you should know about the mechanics of life insurance, the coverage it provides, and the process for receiving benefits if the unexpected occurs.

What is Life Insurance?

Life insurance, also referred to as term life insurance or death cover, offers a lump sum payment to your chosen beneficiaries upon your death. This payout can help your loved ones cover various expenses, including mortgage payments, debts, childcare and school fees, and everyday living costs.

Some policies also provide terminal illness cover, which pays a lump sum if you are diagnosed with a terminal illness and have a limited life expectancy. Life cover can be purchased on its own or combined with other insurance types, such as total and permanent disability (TPD), trauma insurance, or income protection insurance.

What Does Life Insurance Cover?

Here’s a breakdown of what is typically covered by life insurance policies –

Death Benefits –

Life insurance provides a lump sum payment to your designated beneficiaries upon your death. This payout helps your loved ones manage various expenses, including –

- Mortgage Payments – Covering outstanding balances to keep your home.

- Debts – Paying off credit cards, personal loans, or car loans to avoid burdening your loved ones.

- Childcare and School Fees – Assisting with costs related to childcare and education.

- Everyday Living Expenses – Supporting ongoing costs like groceries and utilities.

Terminal Illness Benefits –

Many policies include terminal illness cover, offering a lump sum if you are diagnosed with a terminal illness and have a limited life expectancy. This payout can help with –

- Medical Expenses – Covering treatment, medication, and palliative care costs.

- Financial Support – Maintaining your family’s standard of living while you’re unable to work.

Accidental Death Benefits –

Some policies offer higher payouts in the event of accidental death, providing extra financial support for unexpected costs.

Additional Considerations –

- Exclusions – Life insurance policies often have exclusions, such as suicide within a specific timeframe after the policy starts. It’s essential to review the Product Disclosure Statement (PDS) for details.

- Policy Structure – Life cover can be standalone or linked with other insurance types, which may offer lower premiums but could reduce overall benefit payouts.

How Will Your Policy Be Structured?

Many superannuation funds in Australia automatically provide a basic level of life insurance to their members, and you may have the option to increase your coverage through your super fund. However, it’s important to note that with superannuation-linked policies, the trustee of the super fund is technically the policyholder. In the event of your death, the trustee receives the benefit from the insurer and then distributes it to your beneficiaries according to your instructions or your estate.

When considering life insurance, you should also evaluate your policy terms. Term life insurance is a popular choice that offers coverage for a specified period, often with options to renew until a certain age. If you outlive the policy term, the coverage expires unless you choose to renew it, which may come at a higher premium. Conversely, whole life insurance, although less common in Australia, provides permanent coverage for your entire life, ensuring continuous protection without the need for renewal.

As you apply for life insurance, the insurer will assess your individual risk through a process called underwriting, which considers factors such as your age, health, medical history, and lifestyle. This assessment will determine whether coverage is offered and what your premium payments will be.

Finally, it’s essential to remember that the structure and features of life insurance policies can vary significantly among insurers. To make an informed decision, compare options from different providers, read the Product Disclosure Statement (PDS) carefully, and consider seeking personalised advice from a financial advisor to determine the most suitable structure for your unique needs and circumstances.

Choose Morgan Insurance Brokers

Let Morgan Insurance Brokers take the stress out of finding the right life insurance policy for you. Our team of life insurance brokers will provide personalised guidance, whether you’re comparing term life and whole life insurance options or need help selecting a reputable provider.

We’ll navigate the intricacies of sourcing a policy tailored to your specific needs, ensuring you have the coverage you need to protect your family’s financial future.

With our deep understanding of the life insurance market, you can trust us to help you make informed decisions that offer you peace of mind and financial security.

Get a Quote

Why Do You Need Life Insurance?

Life insurance is fundamentally about protecting your loved ones and securing what matters most. It provides a promise that those we care about will be supported financially if we are no longer able to provide for them. In times of emotional distress, it serves as a source of stability and reassurance for families facing challenging circumstances.

What is Life Insurance

Life insurance is a contract that provides financial protection for your loved ones in the event of your death. When you take out a policy, you pay regular premiums to an insurance company, which in return agrees to pay a lump sum, known as a death benefit, to your designated beneficiaries upon your passing.

This money can be used to cover various expenses, including mortgage payments to help your family stay in their home, everyday living costs such as groceries and bills, outstanding debts like loans or credit card balances, and funeral expenses to ease the financial burden of arrangements.

Life insurance is often regarded as a vital component of financial planning, particularly for individuals with dependants who rely on their income.

Term Life vs. Whole Life Insurance – Which One Should I Get?

Term life insurance provides coverage for a specific period, such as 5, 10, or 15 years. It pays a death benefit to your beneficiaries only if you pass away during the policy term. This type of insurance is generally more affordable than whole life insurance, especially for younger individuals. However, once the term expires, you need to renew it, often at a higher premium.

In contrast to term life insurance, whole life insurance is a permanent life insurance policy designed to provide coverage for the policyholder's entire life, up to a predetermined expiry age or until canceled by the policyholder. This type of insurance is typically more suitable for individuals seeking permanent, consistent coverage

When deciding on what type is insurance for you, here’s a list of questions to consider asking yourself –

- What are your key concerns or priorities when thinking about life insurance? (e.g. affordability, long-term coverage, leaving an inheritance)

- Do you have dependents who depend on your income? (e.g. spouse, children)

- Do you have substantial financial obligations? (e.g. mortgage, debts)

Keep in mind that the ideal type of life insurance varies based on your individual needs and circumstances. Consulting a financial advisor can help you evaluate the advantages and disadvantages, enabling you to make a well-informed choice.

When Should You Buy Life Insurance?

While the concept of life cover is straightforward, not all policies are created equal. Here are a list of factors to consider when selecting life cover and establishing your policy.

Age and Health Status

Premiums are generally lower when you’re younger and in good health. Non-smokers may also qualify for lower rates. Some policies for seniors may not require a medical exam.

Dependents

Consider whether you have dependents, like a spouse or children, who rely on your income. Life insurance can replace your income and provide financial security for them in the event of your passing.

Financial Obligations

Assess your current financial responsibilities, such as a mortgage, credit card debt, and living expenses. Life insurance can help cover these obligations if you were to die or become terminally ill.

Life Events

Major life milestones, such as buying a home, getting married, or starting a family, often increase financial responsibilities. Life insurance can serve as a safety net during these transitions.

Existing Insurance Coverage

Check if you have coverage through your superannuation fund or other policies. You may be able to increase your cover through your super fund. If switching super funds, verify your coverage options, especially if you're over 60 or have pre-existing conditions.

Policy Features and Costs

When comparing policies, consider benefits, coverage terms, exclusions, waiting periods, premium costs, and the potential for future increases. Always read the Product Disclosure Statement (PDS) carefully to understand what is covered and any limitations.

How Morgan Insurance Brokers Can Help

Let Morgan Insurance Brokers find and manage the ideal life insurance policy for you. Whether you're weighing the options between term life and whole life insurance or need assistance choosing a provider, our life insurance experts are dedicated to delivering personalised solutions tailored to your needs.

We handle all the complexities of sourcing a life insurance policy, allowing you to relax and enjoy the peace of mind it provides. With our extensive industry knowledge, you can feel confident that you’re making informed choices for your financial security

Get a Quote

Is It Good To Invest In Life Insurance?

Life insurance is primarily a safety net rather than a traditional investment aimed at generating financial returns. Its main purpose is to provide peace of mind, ensuring financial security for your loved ones. Although some policies may include a cash value component, this is less common in Australia, with a greater emphasis placed on the death benefit.

When considering whether life insurance is suitable for you, take into account factors such as whether you have dependents who rely on your income, the amount of debt you carry, and your overall financial goals. There are various types of life insurance available, each designed to meet specific needs.

Why Should You Invest In Life Insurance?

Determining whether life insurance is a worthwhile investment depends on your individual circumstances, priorities, and financial goals.

When Life Insurance Makes Sense –

Financial Dependents

If you have a spouse, children, ageing parents, or others who rely on your income, life insurance is often crucial. It replaces your income, helping them maintain their standard of living and cover essential expenses.

Debt Management

Life insurance can prevent your debts from becoming a burden on your family. The death benefit can be used to pay off mortgages, loans, and credit card balances.

Future Planning

Life insurance can assist in achieving financial goals for your family, such as funding education, leaving an inheritance, or supporting a charitable cause.

Factors Affecting Value –

Age and Health

Younger, healthier individuals typically pay lower premiums, making life insurance more cost-effective over time. As you age, premiums rise, and pre-existing health conditions can increase costs.

Lifestyle

Factors such as smoking, high-risk occupations, or dangerous hobbies can lead to higher premiums, affecting the overall value of the policy.

Policy Type

Different types of life insurance (e.g., term, whole life) come with varying costs and benefits. It’s essential to assess which type aligns best with your needs and budget.

Alternatives To Consider –

Savings and Investments

If your main goal is to build wealth, traditional investment options may be more appropriate. However, these come with market risks, unlike the guaranteed payout of a life insurance policy.

Superannuation-Linked Insurance

Many Australian superannuation funds provide life insurance as a group benefit, often at lower premiums compared to individual policies. However, these group policies may lack customization and flexibility.

Understanding the complexities of life insurance—such as the various policy types, coverage levels, and potential tax implications—can be difficult. It’s advisable to consult a financial advisor for personalised guidance tailored to your specific financial situation and goals. They can assess whether life insurance is a beneficial part of your overall financial strategy and help you identify the most suitable options.

How To Decide If Life Insurance Is Right For You?

Step 1: Assess Your Needs

Begin by carefully analysing your current situation. Consider your financial obligations, such as mortgages, loans, or credit card debts, and evaluate your family circumstances, particularly if you have dependents who rely on your income. It is also important to review any existing insurance coverage you may already have. This initial assessment will help you understand your specific needs.

Determine whether the default coverage provided by your superannuation fund is sufficient. Many people overlook this aspect, so it’s crucial to assess whether you need additional insurance to adequately protect your loved ones.

Step 2: Explore Your Options

Once you’ve assessed your needs, the next step is to explore your options. If you choose to consider life insurance within your superannuation, do not simply accept the default coverage. Instead, take the time to compare it with other policies available in the market. Pay attention to factors such as coverage limits, benefit payouts, and any additional features that may enhance your protection.

Step 3: Seek Expert Advice

Consulting an advisor or broker is essential for making informed decisions about life insurance products. An advisor can provide personalised insights and help you understand the pros and cons of various options in relation to your policy. This guidance is invaluable in ensuring that you select a policy that aligns with your specific needs.

Step 4: Conduct Regular Reviews

Life is ever-changing, making it vital to conduct regular reviews of your insurance coverage. This ensures that your policy remains aligned with your evolving needs. Major life events, such as family growth, asset acquisition, or changes in health, can significantly alter your insurance requirements. Regular assessments will help you adjust your coverage accordingly.

Let Morgan Insurance Brokers Help You Find The Best Policy

Let Morgan Insurance Brokers simplify your search for the right life insurance policy. Our expert team will provide personalised guidance, whether you’re comparing term life and whole life options or selecting a reputable provider.

Get a Quote

Is it Worth Having Income Protection Insurance?

Is It Worth Having Income Protection Insurance?

Income protection insurance offers a tax-free monthly income replacement if you are unable to work due to injury or medical reasons. This coverage includes benefits for both mental health issues, like stress-related conditions, as well as physical ailments such as back pain, cancer, or stroke.

You may be thinking “is income protection insurance really worth it?” Well, with income protection insurance, you gain peace of mind knowing that you have a financial safety net to cover your bills during periods of illness or injury. Depending on the policy, coverage continues until you either return to work or reach retirement age.

Here’s how it works –

Coverage – The insurance typically covers up to 70% of your pre-tax income. However, some insurers may have a monthly cap on the maximum amount they pay out.

Waiting Period – There’s a waiting period between when you become unable to work and when the payments begin. Longer waiting periods often result in lower premiums.

Benefit Period – The benefit period is the length of time the insurance company will provide payments, usually ranging from two to five years or until you reach a certain age, like 65.

Premiums – The cost of premiums depends on factors such as your age, occupation, health, lifestyle, the coverage amount you choose, the waiting period, and the benefit period.

Exclusions – The insurance doesn’t typically cover situations like deliberate self-harm, suicide attempts, normal pregnancy and childbirth, war, or criminal activities.

Get a QuoteWhen is it Worth it?

Here are some scenarios where income protection insurance is worth considering –

When you have limited savings and/or dependents

If you have limited savings and people who rely on your income, income protection insurance can help maintain financial stability and cover essential expenses like rent or mortgage payments, groceries, utility bills, etc.

When you are self-employed or a casual worker

If you are self-employed or a casual worker without access to sick leave or paid time off, income protection insurance becomes even more critical. It replaces the income you would lose due to an illness or injury, ensuring you can still manage your financial obligations.

According to the Australian Bureau of Statistics (ABS) as of August 2023, there are 1 million independent contractors in Australia who may not have access to sick leave. Additionally, 2.7 million employees (22% of all employees) are not entitled to paid leave. These figures highlight significant aspects of the Australian workforce and their working conditions and how income protection insurance can play a vital role in protecting the workers of Australia.

Get a QuoteWhen you have debts and financial obligations

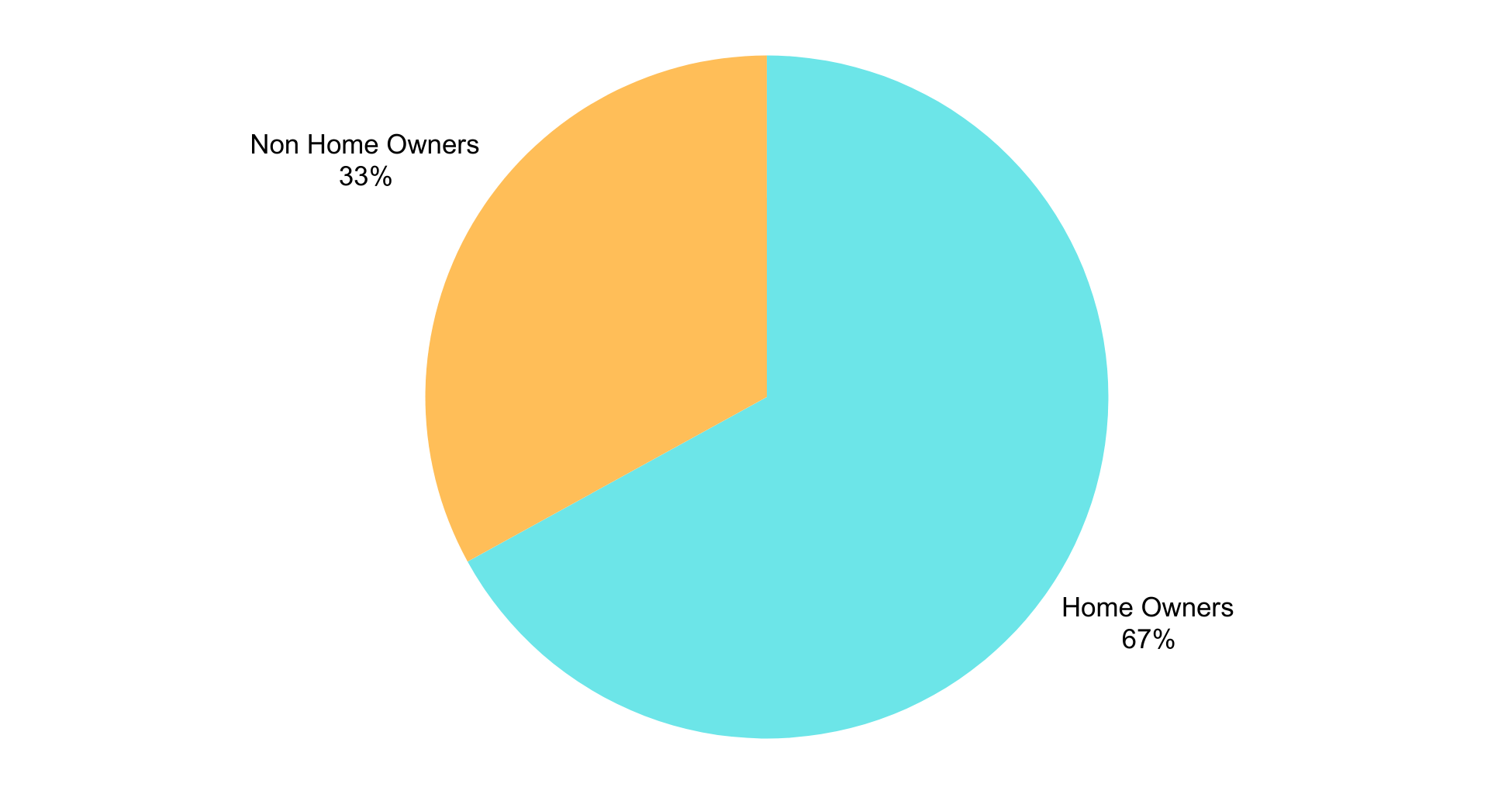

If you have major financial obligations such as a mortgage or rent, car loans, or credit card debt, income protection insurance can help you stay on top of your repayments. It provides a financial buffer, reducing the risk of defaulting on your loans and potentially facing financial difficulties. According to the Australian Bureau of Statistics (ABS), 66% of Australian households own their home, either outright or with a mortgage. This high rate of homeownership shows the importance of income protection insurance. For homeowners, maintaining mortgage payments is crucial to avoid financial distress or even foreclosure in the event of an unexpected illness or injury.

When you work in a high-risk occupation

If your job involves physical labour, operating machinery, or other high-risk activities, the chances of work related injuries are higher. Income protection insurance can be beneficial in such occupations, offering financial support during recovery.

When is it No Longer Worth it?

While income protection insurance offers valuable financial security, there are certain situations that make it less of a priority.

Sufficient savings and low expenses

If you have a sufficient emergency fund or minimal expenses, and can manage financially for an extended period without your regular income, income protection might be less crucial. This is particularly relevant if you have low or no debts and have no dependents.

Nearing retirement with ample savings

If you’re nearing retirement and have substantial savings, income protection will seem less appealing. Instead of paying premiums, you might choose to retire early if faced with a sudden health event, choosing to utilise savings for financial support.

Low-income earners

If you’re a low income earner, you might not find income protection insurance appealing compared to other types of insurance like Total & Permanent Disability insurance insurance which offers a payout if you are permanently unable to work, regardless of your earnings. This is because income protection insurance often replaces a portion of your income which might not be substantial for low-income earners.

Why Choose Morgan Insurance Brokers?

At Morgan Insurance Brokers, our team brings extensive experience, knowledge, and expertise in the insurance industry.

We recognise that obtaining the right income protection insurance can be challenging, particularly when looking for thorough coverage from a reliable provider. That’s why we’re committed to identifying the best coverage and pricing that fits your individual requirements. With connections to major insurers, our experts are here to help you navigate your choices and make an informed decision.

Our aim is to assist you in managing your rent or mortgage, handling everyday expenses, and ensuring you don’t have to depend on friends, family, or other sources for financial aid.

Get a Quote