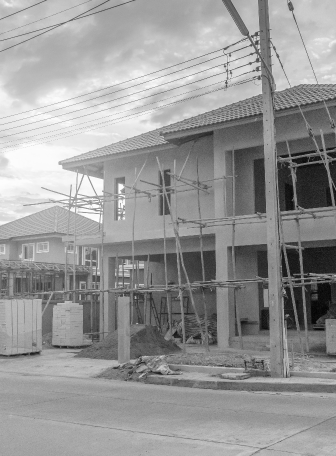

Is your residential investment secure?

Is your residential investment secure?

Purchasing an investment property is a very exciting time. Growing your portfolio can provide many financial benefits, from passive income to tax advantages, and are also a great long term wealth strategy if the value of the property increases during the period of ownership.

From the moment you sign the contract, are a whirlwind of tasks that need to be executed. Conveyancing, contracts, building and pests, loan approval, insurances, the list goes on.

With all the excitement and time pressure surrounding this process, it’s easy to see how purchasing insurance can become rushed, resulting in potentially inadequate cover.

Protecting your investment with Insurance

Protecting your investment with Insurance

Insurance is the most vital process when purchasing an investment. It will protect what you’re trying so hard to achieve – a positive rental income.

There are so many aspects to a Landlords Insurance policy than just insuring the building. These are explored below.

Rent default:

Rent default is when the tenant falls behind in their rental payments without giving any written or verbal nature. This section also can include legal and court costs to pursue recovery of the arrears.

Theft by Tenant:

Theft by Tenant will protect your contents items by theft from your tenants. If your property is leased unfurnished, it can protect your fixtures and fittings. Curtains/blinds etc.

Loss of Rent:

Loss of Rent will protect your rental income for 12 months where your insurer deems your property unfit for your tenants to live in.

Accidental damage:

An Accidental damage policy will extend to cover your property from Accidental damage caused by tenants. This not a standard cover for most insurers, however it is vital. Morgan Insurance Brokers offer this cover as our policies that we source have had this cover negotiated in.

Landlords Liability:

Public Liability Insurance comes standard in a Landlords Insurance policy. It covers the Landlord for costs associated with a personal injury or property damage claim that they’re found liable for. This cover also extends to the tenants and their guests.

Each insurer’s policies contain vastly different terms, conditions, sublimits, and excluded covers. Its extremely important to review each quote you obtain to ensure that the level of cover is going to protect your investment.

Pricing:

Pricing should not be a driving factor for a policy like this as you could find yourself under insured and out of pocket if you are selective with the important additional covers mentioned above.

Benefits of using a broker:

Engaging an insurance broker to guide you through this exciting time is going to provide you with sound advice and peace of mind that you’re adequately covered to minimise the financial impact if you ever suffered an insured event.

Brokers can source a comprehensive policy at a competitive price without having to forego these important covers.

What to do if you’re involved in a motor vehicle accident

What to do if you're involved in a motor vehicle accident

If you unfortunately find yourself in a car accident, below are some points of action that protect you financially.

Make sure everyone is safe

First of all, if you’ve been in an accident, make sure you’re safe and not injured, along with your passengers, and others in the other vehicle. If so, assess the injuries and make a determination if an ambulance should be called.

If there were no injuries to any person’s, then if it’s safe to exit the vehicle, do so.

Make sure the vehicle has moved into a safe area off the road to avoid any further damages or injuries.

Assess the damages

When you’ve exited the vehicle, assess the damages. Is it drivable? Will you need a tow truck? If you need a tow truck, call a local company and let them know your pick up destination. You can have them deliver your vehicle to a near by smash repairer, your home address, or their holding yard. Please note that holding yards can charge a daily storage fee.

Obtaining and recording the details of the accident

Now, here is the most important part. Obtaining the information of the other party. It is crucial (especially if you believe you were not at fault for the damages) that you document as much as possible, including the other vehicle and drivers details.

Important information check list

- Vehicle make and model

- Registration

- Driver name

- Driver telephone contact number

- Copy of the other drivers licence (take a photo front and back)

- Driver’s home address

- Driver’s contact number

- Photos of the other vehicle including registration plates in the photo

- Insurer Name and policy number (or claim number)

- Address of accident

- Write down a brief description of the events and who was at fault

Engaging your Insurance Company

With this information, your Insurance Company will be able to contact the other party and ask them for their insurance details, including who they are insured with and what their claim number is. This aids in a successful recovery of any claim amounts that your insurer paid for the repairs of your vehicle. Withthis information, your Insurance Company will be able to contact the other party and ask them for their insurance details, including who they are insured with and what their claim number is. This aids in a successful recovery of any claim amounts that your insurer paid for the repairs of your vehicle.

Without this information, your insurer may not waive your excess, and may find you technically “at fault” if there is an unsuccessful recovery in claim payments. This will go on your claims history and could impact your premiums for years to come.

Notifying your Insurance broker

If you are insured through a Broker, contact them and provide them with this information to enable them to lodge a claim on your behalf.

Getting your vehicle repaired

The next step is to have your vehicle repaired. Usually, you would have your vehicle quoted and assessed and then the repairs subsequently approved. Depending on when the repairer can book you in, you could be waiting for a few weeks until a repair date. If this is the case, contact your Insurance Broker to see if you’re eligible for a hire car under your policy. If you’re insured directly, contact your insurer and query your policy coverage for the use of a hire car.

Once your vehicle is repaired, ensure you’re happy with the quality of the work, then happy driving!

In summary, here are the action points

- Make sure everyone is safe

- Move vehicle to a safe area

- Organise a tow truck if needed

- Obtain drivers information

- Take photos

- Contact Broker or Insurer to lodge claim

- Take vehicle in for a quote for repairs

- Book in and attend repair date

Claims can be stressful and time consuming. You could have difficulties with dealing with the other parties, long wait times on hold with insurers, delays with repairs, and pressure finding alternative transport whilst your vehicle is getting fixed.

Our free claims handling would include the below services, but not limited to;

- Lodging the claim with the insurer

- Speaking to the third party driver

- Facilitating tow trucks and repairs of vehicle

- Organising hire car

Please contact Morgan Insurance Brokers for a Motor Vehicle Insurance quote.

We hope the above can assist in the event of a car accident.

The ins and outs of Business Insurance 2022

The ins and outs of Business Insurance

What is business insurance?

A business takes years to build – but an accident or disaster could destroy it all in minutes. That’s why businesses should help protect themselves with a quality business insurance pack.

With the right cover in place, owners can run their business with confidence, knowing that their premises, stock, equipment and reputation are protected by insurance.

Who should consider it?

Business owners can benefit from taking out an affordable and comprehensive business insurance pack to help protect them against the main risks involved in running a business.

What can it cover?

Business insurance packs can offer general protection for a business, which may include cover against:

Property Damage

Repair or replacement of property damaged.

Business interruption

Loss of trading profit following insured damage to property and additional costs and expenses incurred during a claim.

Theft

Repair or replacement of property stolen.

Money

Loss of money. Excludes electronic funds.

Public or products liability

Your liability to pay compensation for personal injury and property damage as well as the costs involved in defending a claim triggered by the policy.

Glass

For replacing glass inside or outside your premises, including your shopfront windows, mirrors or display cases.

Transit

For stock that is in transit on the road, in the air or by sea.

Electronic equipment breakdown

For repairing or replacing electronic equipment that breaks down.

Machinery breakdown

Cover for costs associated with machinery breakdown.

General property

To cover your tools of trade, including laptops and tools that you use for your profession or trade.

Tax audit

To cover the costs of being audited by the ATO.

Employee dishonesty

Direct financial loss of the business caused by the dishonest or fraudulent conduct of an employee which is first discovered during the period of insurance.

“Having the right insurance will help protect your business and minimise its exposure to risk. This may include insuring your business, your income and your commercial risk.”

Contact one of our insurance specialists at Morgan Insurance Brokers for your tailored Business Insurance Quote.